GOVERNANCE AND THE BARAKA OF CONVENING - What Five Years of Global Conferences Have Built — and What the Next Five Can Make Auditable

Abstract. Across five years and four regions, the global Islamic finance conference circuit has built something that did not exist a generation ago: a coherent public-facing surface through which the industry presents itself to regulators, capital, scholars, and the wider public. That visibility is itself a governance achievement. The next phase is auditability — making the public square the floor on which governance evidence becomes legible, comparable, and priced. Three disclosure instruments — public Sharī‘ah health scorecards, maqāṣid benchmarks, and retail governance disclosure templates — meet the minimum credible disclosure threshold the next phase requires. The standards are written. The institutions are convened. The opportunity now is to make visibility auditable, and the institutions positioned to lead this phase are the ones that built the last.

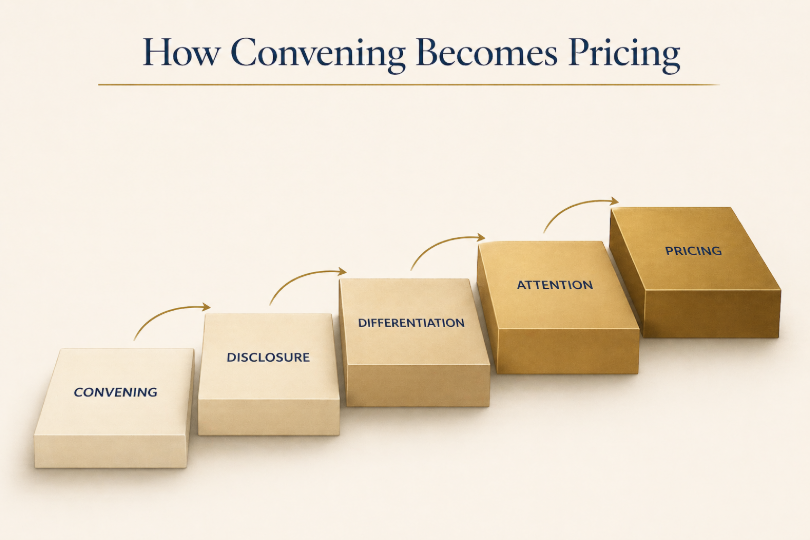

Five years of convening built visibility. The next five can make visibility auditable.

I. The Conference Floor Is the Industry’s Public Square

A thirty-year story of Islamic finance has been told across the conference programs of the GCC, Southeast Asia, Europe, and North America. From Manama to Kuala Lumpur, London to Boston, the circuit has produced a coherent public-facing institutional surface where one did not previously exist.

The names are familiar: the World Islamic Banking Conference, the IFSB Annual Summit, the Global Forum on Islamic Economics and Finance, the IFN Asia and Europe Forums, the Indonesia Sharia Economic Festival, the London Sukuk Summit, the Harvard Islamic Finance Conference, and the World Bank–IsDB Inclusion Forum. From 2019 through 2024, these gatherings built thematic convergence, regional density, and a shared institutional vocabulary across four geographies that did not previously share one.

That visibility is itself a governance achievement. A public square is the threshold condition for public accountability — and the convening circuit has built it.

The first five years built the public square. The next five build what happens on it. The first paper in this series [View] established that governance quality is the primary pricing variable in Islamic capital markets. The mechanism connecting the convening circuit to that variable is observable: conference disclosure norms produce repeated public comparison; public comparison produces reputational differentiation; reputational differentiation attracts allocator attention; allocator attention is priced.

Convening is therefore not adjacent to pricing. It is upstream of it. The institutions that built the circuit have built the surface on which the next phase of governance work becomes possible — and they are well-positioned to lead it.

A public square is the threshold condition for public accountability. The circuit has built it.

II. Five Years of Convergence

Across the circuit’s last five years, four substantive theme clusters have emerged: fintech and digital Islamic banking; ESG and green sukuk; inclusion and social finance; and regulation and standards alignment. A fifth — ethical branding and faith-finance narrative — runs alongside them. Together, these clusters have produced the audience, vocabulary, and momentum that make the next phase actionable.

Fintech and digital Islamic banking moved from peripheral panels in 2019 to plenary themes by 2024. The IFSB’s working paper on regulatory practices in digital Islamic banking, alongside its earlier fintech landscape work, has set the framework. The next phase is moving from framework to disclosed institutional practice — Sharī‘ah ICT standards that operate at the level of audited compliance, not aspirational positioning.

ESG and green sukuk built scale across Europe and the GCC. The London Sukuk Summit and WIBC have hosted significant issuance announcements; Luxembourg and U.K. policy frameworks have integrated Islamic instruments into sustainable-finance taxonomies. The next phase is the convergence of Sharī‘ah and ESG measurement architecture — a unified taxonomy that allows an issuance to be evaluated against both at once, rather than retrofitted to either.

Inclusion and social finance have been the structural achievement of Southeast Asia. Zakat, waqf, micro-takaful, and women’s economic participation now sit within a coherent inclusion architecture aligned with maqāṣid principles. The Indonesia Sharia Economic Festival and the World Bank–IsDB Inclusion Forum have helped build that architecture. The next phase is the integration of zakat–waqf–sukuk chains as measurable instruments of poverty relief, supported by disclosure standards that allow capital to follow performance.

Regulation and standards alignment is the cluster where the circuit has most visibly hosted AAOIFI’s continuing work, IFSB-10’s Sharī‘ah governance framework, and the supervisory trajectory now formalized in IFSB-31. The standards exist. The next phase is implementation visibility — the convening stage as the public face on which standards adoption is reported, not only discussed.

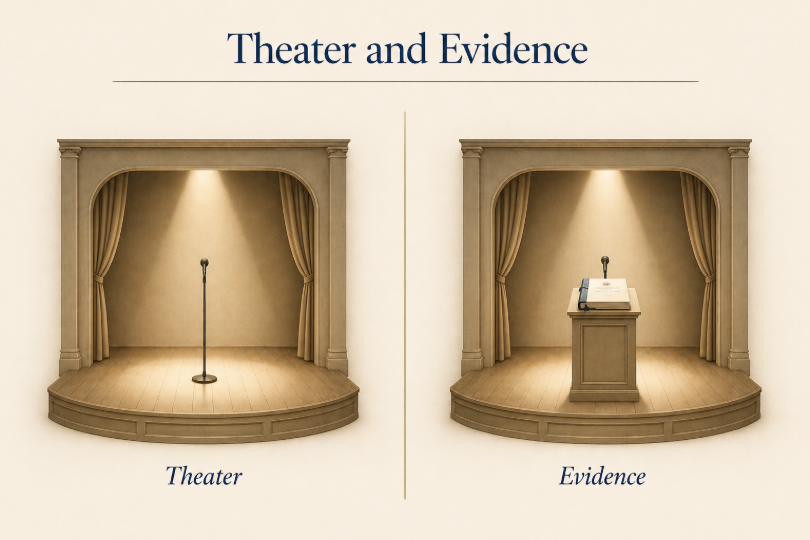

The convergence is the period’s achievement. It is also the condition that makes the next risk legible. Not every panel produces governance. Some produce only convening theater — themes repeated without measurable disclosure, panels that substitute for audit, recognition that substitutes for reporting.

Convening theater is the cousin of the symbolic compliance documented in the second paper of this series [View]. Both produce the appearance of oversight without the structure of it. The risk for the next five years is not that the circuit fails to grow. It is that convening becomes a substitute for evidence rather than the surface on which evidence appears.

III. Regional Topologies and Their Complementarity

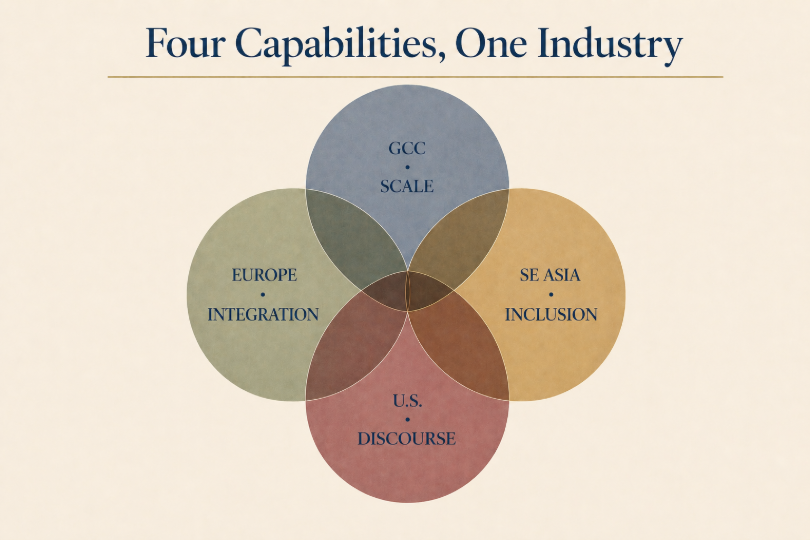

Each region has built a distinct governance capability. Read together, the topology reveals four contributions awaiting integration — and the convening circuit is positioned to host that integration.

The GCC has built scale. WIBC, the IFSB Annual Summits hosted across Bahrain, Kuwait, and Jeddah, and the region’s Sharī‘ah governance councils have produced the institutional density that allows Islamic finance to operate at sovereign and corporate scale. The capability the GCC contributes is institutional infrastructure for public Sharī‘ah health reporting at scale. What other regions have begun, the GCC is positioned to operationalize.

Southeast Asia has built inclusion. The Malaysian Islamic finance ecosystem, Bank Negara Malaysia’s regulatory leadership, and Indonesia’s retail and policy infrastructure have produced a coherent inclusion architecture across the global circuit. The capability Southeast Asia contributes is governance literacy across the practitioner pipeline. The second paper in this series established that governance literacy is built where it is taught, and Southeast Asia teaches it most systematically.

Europe has built integration. The London Sukuk Summit, the IFN Europe Forum, and the U.K. and Luxembourg policy architectures have produced a working integration between Islamic finance and conventional sustainable-finance frameworks. The capability Europe contributes is standards translation — ESG, regulatory parity, and sustainability taxonomy convergence that allow Islamic finance to operate without translation friction in Western capital markets.

The United States has built discourse. The Harvard Islamic Finance Conference and cross-disciplinary academic engagement around Islamic finance and ethics have contributed a distinct discourse capability: translating Islamic finance debates into the institutional vocabulary of Western academic and regulatory audiences. The capability the U.S. contributes is regulatory and standards research that turns discourse into institutional design.

Four regions. Four capabilities. Integration is the next phase of the work — and the convening circuit is the surface on which that integration becomes possible.

The GCC built scale. Southeast Asia built inclusion. Europe built integration. The U.S. built discourse. The next five years can build the convergence that makes them one industry.

IV. The Agenda the Next Five Years Can Build

Three disclosure instruments meet the minimum credible disclosure threshold the next phase requires. Each operationalizes standards already written and increasingly formalized by institutions the convening circuit already gathers. The materials exist. The audience exists. The next phase is making them operational on the convening stage.

Public Sharī‘ah Health Scorecards. AAOIFI’s external Sharī‘ah audit standard (ASIFI 6), alongside IFSB-31’s supervisory framework, provides the architecture. A scorecard turns that architecture into comparable annual disclosure: board independence and rotation, fatwa documentation and minority opinion records, internal audit findings and resolution status, conflict-of-interest disclosure, and Sharī‘ah non-compliance income and purification.

Stress-test results sit alongside ESG dashboards. Sharī‘ah governance becomes legible at the institutional level. The convening circuit is the natural distribution surface — the floor on which scorecards are released, compared, and discussed.

Positive Screening and Maqāṣid Benchmarks. Negative screens — what an investment must avoid — have been the field’s operational baseline for thirty years. The next phase is positive screening: indices and benchmarks aligned with maqāṣid al-sharī‘ah that measure what an investment actively contributes to the higher objectives the tradition names — the preservation of life, intellect, lineage, wealth, and faith — not only what it avoids.

A maqāṣid benchmark requires disclosed methodology: the criteria applied, the evidence required, the weightings used, and the review process. Disclosure is what makes the benchmark auditable rather than asserted. The convening circuit is positioned to host both the AAOIFI–ESG taxonomy convergence and the methodology disclosures that allow these benchmarks to function as evidence rather than positioning.

Retail Governance Disclosure Templates. AAOIFI Governance Standard 21 provides a foundation for Sharī‘ah Supervisory Board review and reporting. The next phase is translating those institutional reporting norms into retail-grade disclosure — standardized templates that present, in usable form, the same governance information available to a sovereign allocator. Templates make disclosure portable, comparable, and enforceable as a sector norm. The convening circuit is positioned to host the policy and practice work that defines them.

This argument builds on the convening leadership already provided by IFSB, AAOIFI, IFN, REDmoney, WIBC, and the academic conveners whose cumulative work has made this next phase possible. These instruments are operationalizations of the standards those bodies have established — extensions of their work, not corrections of it.

The standards are written. The audience is convened. The next five years are the activation.

V. The Baraka of Convening

The Arabic root jam‘ — gathering — runs through the institutional vocabulary of Islamic civilization. Jum‘ah, the Friday congregation. Ijmā‘, the scholarly consensus through which legal questions are resolved. The conference circuit, in its institutional function, is a continuation of that tradition: bringing practitioners, scholars, and capital allocators into the same physical and intellectual space, where shared work becomes possible.

The first paper in this series [View] established that governance quality is what Islamic capital markets price. The second [View] established that governance literacy is what the practitioner pipeline must build. The third [View] established that governance architecture must be embedded in the systems institutions rely on. This paper adds a fourth dimension: governance must be auditable in public — and the convening circuit is the floor on which that auditability can happen at scale.

Three requirements follow. They are framed not as critique of the circuit’s last five years, but as the work the next five are ready for.

Independence. The convening circuit is positioned to formalize the structural separation between sponsorship logic and agenda-setting authority, raising the governance observability threshold above the point at which sponsorship can shape what is governed in public. AAOIFI, IFSB, national Sharī‘ah advisory councils, and academic conveners are well-placed to anchor this evolution. The opportunity is to make agenda-setting a visibly independent function alongside the commercial logic that funds the gathering — preserving both, and protecting each from the other.

Transparency. The circuit is positioned to host what institutions are increasingly ready to disclose. Public Sharī‘ah audit scorecards, SSB independence reporting, and IFSB-31 disclosure norms can become regular features of the convening stage rather than exceptional ones. The institutions that lead in this disclosure will set the standard the rest of the industry follows — not through advocacy, but through example.

Accountability. The circuit is positioned to make governance performance publicly legible — clearing the participation threshold that distinguishes a market in which governance is observed from one in which governance is only claimed. Standardized disclosure formats, year-over-year reporting, and recognition mechanisms for institutions whose practice meets ratified standards are within reach. Accountability that is publicly visible becomes accountability that is publicly priced.

These requirements are not aspirational. They are operationally available, and the institutions positioned to build them are the ones that built the last five years of the circuit.

The first paper in this series documented what governed Islamic capital markets produce: tighter spreads, deeper participation, and long-run credibility that compounds across cycles. The mechanism extends to the convening circuit. An industry whose convening floor is also its evidence floor is an industry whose governance becomes a publicly priced asset rather than a privately held one.

If the convening circuit hosts this evidence layer, it sets the standard the industry is priced against. If it does not, that standard will be set elsewhere — through allocator due diligence, regulatory disclosure mandates, and ultimately, the pricing of governance asymmetry.

The next trillion will be raised by the convening that turns its themes into its evidence.

Authority in Islamic finance is earned by being answerable in public — and the public square the convening circuit has built is the floor on which that answerability now becomes visible.

References

• Siddiqui, R. & Hammad, A. Governance and the Baraka of Trust. Baraka Strategic Advisory Council, 2025. [Article 1 in this series]

• Siddiqui, R. & Hammad, A. Governance and the Baraka of Education. Baraka Strategic Advisory Council, 2025. [Article 2 in this series]

• Siddiqui, R. & Hammad, A. Governance and the Baraka of Guidance. Baraka Strategic Advisory Council, 2025. [Article 3 in this series]

• Accounting and Auditing Organization for Islamic Financial Institutions. Governance Standards, including GS 1 and GS 19–22 on Sharī‘ah Governance. Issued/revised 2024.

• Accounting and Auditing Organization for Islamic Financial Institutions. ASIFI 6: External Sharī‘ah Audit.

• Islamic Financial Services Board. IFSB-10: Shariah Governance Systems for Institutions Offering Islamic Financial Services, 2009.

• Islamic Financial Services Board. IFSB-31: Guiding Principles for Effective Supervision of Sharī‘ah Governance. Adopted July 2025.

• Islamic Financial Services Board. Fintech and Islamic Finance: Current Landscape and Future Outlook. Kuala Lumpur: IFSB, 2020.

• Islamic Financial Services Board. Regulatory Practices in Digital Islamic Banking. Working Paper WP-27, December 2023.

• ICD–LSEG. Islamic Finance Development Report 2025.

• ICMA, IsDB & LSEG. Guidance on Green, Social and Sustainability Sukuk. April 2024.

• Kamali, M. H. Principles of Islamic Jurisprudence. Islamic Texts Society, 3rd ed., 2003.