GOVERNANCE AND THE BARAKA OF TRUST - Why Governance, Not Just Sukuk, Is the Real Engine of Islamic Finance

Abstract: Islamic finance does not have a product problem. It has a governance problem. This paper examines how governance failures — across banking, investing, takaful, and social finance — erode the foundational principles of amanah (trusteeship) and translate directly into pricing penalties, capital flight, institutional exclusion, and long-run performance deterioration. The evidence is institutional, empirical, and accumulating. Governance quality is the dominant non-financial driver of participation, pricing, and performance in Islamic finance. The market has already begun to answer this question. The industry has not.

Islamic finance does not have a product problem. It has a governance problem.

The industry has spent decades refining structures — sukuk, screening ratios, compliance frameworks. It has mastered the documentation. What it has not built, at scale, is institutional trust. And capital is responding accordingly.

The question the industry has consistently deferred is not the what — what is halal, what is haram, what is the structure of the sukuk. The deferred question is the how. How do we ensure that the institution managing your zakat does not squander it? How do we ensure the Sharī'ah board is not a rubber stamp for management's growth ambitions? How do we protect the amanah — the trusteeship — that gives every structure its moral purpose?

The industry is facing a silent crisis. Not a liquidity crisis. A governance crisis. When we strip away the theological framing, Islamic finance is a document-heavy, rules-centric, trust-based industry. When trust is structurally undermined, the economic consequences are neither subtle nor reversible. They are visible in spreads, in deposit flight, in institutional exclusion, and in the growing reluctance of global capital to engage.

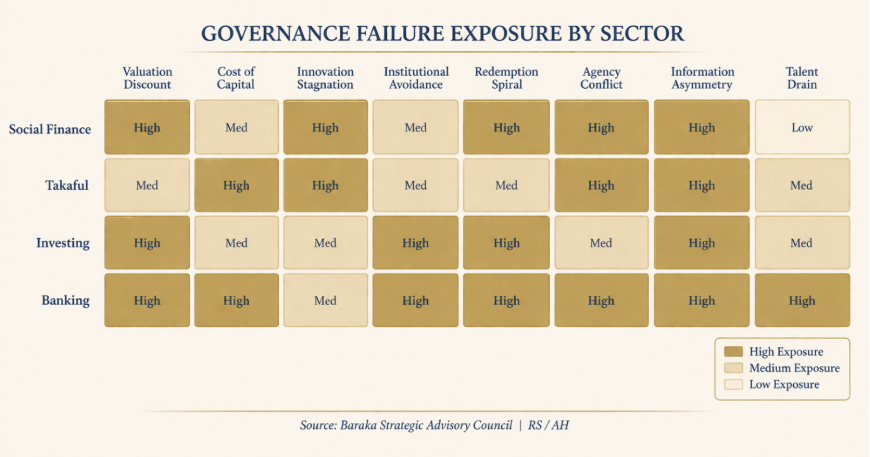

Across every segment of Islamic finance — banking, investing, takaful, and social finance — governance quality is emerging as the dominant non-financial driver of participation, pricing, and long-term performance. What follows is the evidence.

I. Governance Is Priced — Whether Disclosed or Not

Markets price what they can observe, and when Sharī'ah governance is opaque, they price in uncertainty. The result is what practitioners increasingly recognize as the sukuk discount — a spread premium and valuation haircut applied to institutions whose oversight structures are weak, captive, or non-transparent.

The collapse of Islamic Bank Ltd (IBL) in South Africa in 1997 remains the clearest early example. Poor credit risk management, undisclosed riba-based liabilities, and an absence of independent oversight allowed problems to compound until depositor confidence collapsed entirely. The Ihlas Finance House failure in Turkey is a more precisely documented case. When Ihlas — then the largest domestic Islamic finance institution in the country — collapsed in February 2001 due to mismanagement and illiquid assets representing approximately 96% of its deposit ratio, the contagion was immediate and sector-wide: Islamic banking's total market share in Turkey was reduced by 50%, as depositors across all remaining institutions rushed to withdraw funds. The episode directly precipitated the establishment of a national deposit insurance scheme and led to wholesale regulatory reform of the participation banking sector.

The contrast between Dubai Islamic Bank (DIB) and Abu Dhabi Islamic Bank (ADIB) in the late 2000s illustrates the same dynamic at a more granular level. DIB's 2008 fraud case — in which executives embezzled approximately $500 million through fictitious investment structures, resulting in sentences and fines totaling 1.8 billion dirhams in one of the UAE's largest fraud proceedings — triggered prolonged litigation and sustained reputational damage. ADIB, operating under a more rigorous and transparent governance structure, consistently commanded tighter profit rates and greater depositor confidence through the same period of market stress. The market was not evaluating theology. It was evaluating institutional integrity.

The same mechanism operates across the capital structure. When Bank Negara Malaysia imposed an administrative monetary penalty of RM3.445 million on Bank Islam Malaysia Berhad in July 2025 for non-compliance with the Islamic Financial Services Act and related policy documents, the immediate cost was financial — but the larger consequence was heightened institutional scrutiny around governance, controls, and operational resilience. For institutional investors to whom governance disclosure is a threshold criterion, not a secondary consideration, that scrutiny carries a cost well beyond the penalty itself.

In the takaful sector, the IAIS and IFSB have identified corporate governance, transparency, and the clear separation of participant and operator roles as foundational supervisory concerns — gaps that constrain scalability and limit the sector's ability to attract sophisticated institutional capital. IFSB-8, issued as a governance benchmark for takaful undertakings, reflects the extent to which regulators have treated structural governance reform as a prerequisite for industry maturation rather than an optional enhancement. In social finance, development agencies and impact investors have largely withdrawn from waqf and zakat vehicles where stewardship accountability is insufficient. Governance weakness is not a secondary compliance issue; policy bodies such as COMCEC treat it as a development constraint affecting standardization, credibility, and long-term scalability.

Investors are not differentiating between riba and gharar. They see a governance black hole — and they price accordingly.

II. Governance Determines Who Gets Access to Capital

Governance failure does not only impose direct costs — elevated spreads, higher reinsurance premiums, regulatory fines. It also imposes an opportunity cost that is harder to measure but structurally more damaging: stagnation. When boards lack genuine challenge, management optimizes for comfort rather than performance. The result, in a sector already facing disruptive pressure from fintech and conventional ESG capital markets, is an accelerating competitiveness gap.

Malaysia's divergence from the Gulf in the early 2010s is instructive. Institutions like Bank Islam Malaysia and MBSB Bank, operating under Bank Negara Malaysia's governance-driven pressure to innovate, launched the first Islamic digital banks and wealthtech platforms in the region. In contrast, traditional waqf departments across South Asia — insulated from governance accountability — continued to hold prime real estate assets generating sub-2% returns. No one on the board was empowered, or incentivized, to ask the foundational question: what is this asset actually for?

The ESG dimension compounds the problem. Large institutional allocators — including sovereign wealth funds operating under explicit ethical and governance screens — apply exclusion and observation criteria that encompass anti-corruption standards, governance transparency, and public accountability, regardless of product labeling or Sharī'ah compliance status. Institutions lacking independent Sharī'ah audits, transparent oversight, or accountable board composition fail governance screens on structural grounds. The exclusion is not ideological. It is architectural: when governance cannot be demonstrated, it is assumed to be absent — and priced accordingly.

Global funds seeking ethical alpha are not differentiating between Islamic and conventional structures. They are screening for governance quality. Institutions that cannot demonstrate it are being screened out — losing access to precisely the institutional capital that Islamic finance has long sought to attract.

III. How Governance Failures Compound: Spirals, Agency Conflicts, Opacity

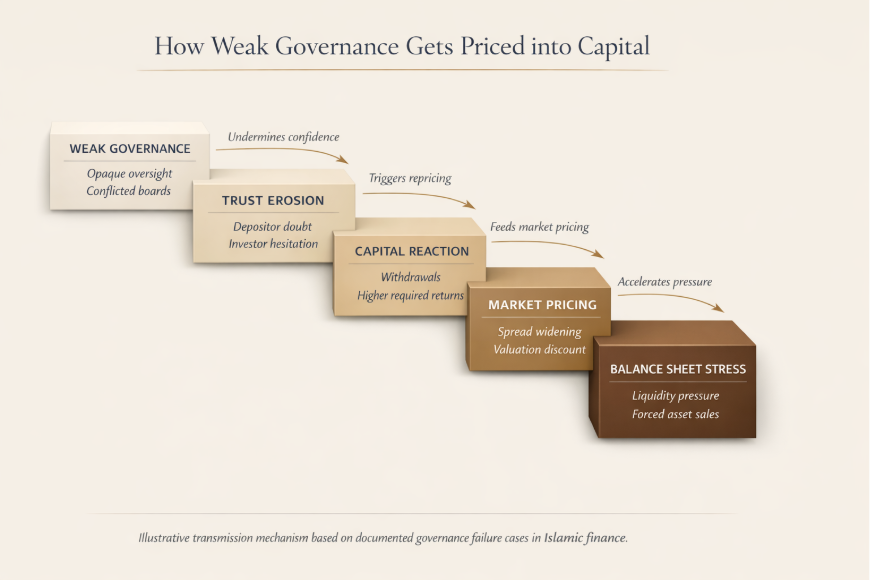

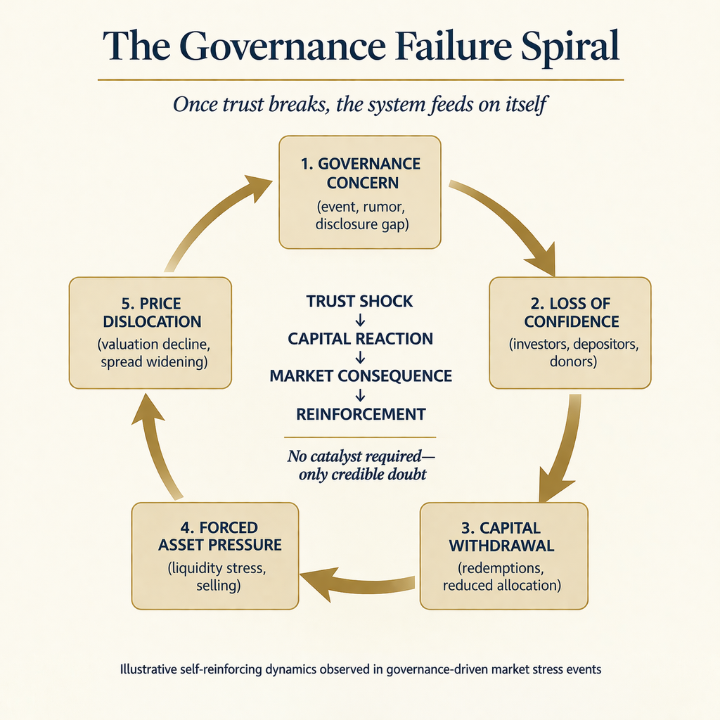

Governance failures are rarely discrete events. They compound. The mechanism is familiar to anyone who has observed a redemption spiral: an initial disclosure or rumor of non-compliance triggers capital flight; capital flight forces asset liquidation at distressed prices; distressed prices validate the original concern and accelerate the outflow. The firewall against this cycle is governance. When that firewall is structurally weak, panic does not require a catastrophic trigger — it requires only a credible rumor.

The Arcapita case in Bahrain — a licensed Islamic wholesale bank and global manager of Sharī'ah-compliant alternative investments — illustrated how quickly governance and liquidity sensitivity can translate into institutional distress. The ASNB-adjacent rumors in Malaysia demonstrated the same fragility at the retail level: where governance transparency is absent, market participants fill the information vacuum with the worst available interpretation. The spiral does not require a catastrophic trigger. It requires only a credible rumor and an institutional architecture too opaque to refute it.

The underlying mechanism in most of these cases is an agency conflict of a specific type: management treating Sharī'ah compliance as a marketing instrument rather than a binding operating philosophy. IBL's management pursued growth through riba-based instruments while presenting a Sharī'ah-compliant face to depositors — a breach of mudarabah duty that destroyed credibility when exposed. HSBC Amanah encountered a subtler version of the same problem: customers and scholars who perceived that the Sharī'ah governance committee was structurally subordinate to the bank's balance sheet objectives began migrating toward fully independent Islamic challengers.

Information asymmetry is the enabling condition for all of these failures. IBL concealed non-performing loans representing 30% of its portfolio and engaged in creative accounting until capital flight forced disclosure. In the takaful sector, policyholders routinely lack transparency on how tabarru' pools are managed and how surpluses or deficits are allocated — a structural opacity that weakens retention and erodes the participant trust that the mutual model depends on. In social finance, donor uncertainty about fund utilization does not merely reduce individual contributions; it produces a self-reinforcing cycle in which diminished confidence leads to reduced oversight pressure, which leads to further governance deterioration.

The social finance dimension makes this structural dynamic most visible. A consistent body of empirical literature — anchored in Indonesian and Malaysian zakat institutions — finds that governance quality, transparency, and accountability are the dominant determinants of public trust in zakat organizations, and that muzakki distrust directly causes donors to stop giving to those institutions entirely. Institutions that consistently report finances openly demonstrate more stable and efficient collection performance than those that do not. The causal chain is not circular: governance precedes trust, and trust precedes giving. When that chain breaks — as it has in documented cases involving private amil zakat bodies in Indonesia — the institution does not merely lose revenue. It loses legitimacy, which is not a financial variable and does not respond to financial remedies. It recovers on a generational timeline, if at all.

IV. Governance Is Not a Compliance Variable. It Is a Pricing Variable.

The most consequential long-run effect of governance failure is one that rarely appears on a balance sheet: the systematic departure of the people best positioned to reform the institution. Ethical finance professionals — scholars, actuaries, structurers, compliance officers — do not remain in environments where Sharī'ah boards are compensated based on the volume of products they approve, or where board composition reflects family relationships rather than expertise. They leave. And they do not return.

The directional pattern is visible at the credit rating level. Cross-country research across Asian Islamic banks finds that governance-related characteristics — board independence, board expertise, and Shariah board expertise — are positively associated with credit ratings, while CEO power and concentrated ownership structures are negatively associated. The same research finds that credit ratings are materially and consistently higher for Southeast Asian Islamic banks than for GCC counterparts, a differential the authors attribute in significant part to governance framework differences between the two regions. This is not a theoretical proposition. It is a measurable, published pricing gap between governance-credible and governance-weak jurisdictions.

The performance literature is more nuanced than a simple "governance improves returns" summary but points consistently in one direction. Some studies of AAOIFI governance disclosure find insignificant short-run relationships with ROA and ROE — a result that is accurate but incomplete. Studies that examine governance quality more comprehensively — including board structure, audit committee effectiveness, and Shariah supervisory board characteristics across MENASA Islamic banks — find that these governance variables have positive and significant associations with both ROA and ROE. A global study of 180 Islamic banks across 56 countries over the period 2010–2019 found that Shariah Advisory Board size, meeting frequency, and the active presence of Shariah advisers all improved financial performance. The emerging consensus is not that governance always produces short-term alpha. It is that governance quality is a structural prerequisite for long-run institutional stability — and the evidence is accumulating.

The Tabung Haji crisis in Malaysia between 2017 and 2018 is, in this sense, the most complete case study available: governance failure produced financial distress that required government intervention; post-intervention governance reform is now, measurably, rebuilding both performance and depositor confidence. The sequence is not coincidental. Accountability and capital preservation are not competing objectives. They are the same objective.

The alpha gap is real. Institutions with strong governance attract better talent, lower their cost of capital, access a broader institutional investor base, and generate more stable returns over time. Those without it do not merely underperform — they create structural liabilities that accrue silently until they become acute.

V. The Baraka of Governance

Islamic finance has spent sixty years perfecting the legal architecture to avoid riba and gharar. That work matters. But it has been pursued at the expense of the amanah — the trusteeship — that gives the architecture its purpose. A structurally sound sukuk issued by an institution with a captive Sharī'ah board, opaque fund management, and family-dominated oversight is not a safe instrument. It is a compliant one. The distinction is no longer academic.

Governance quality is now the single largest non-financial driver of participation and performance in Islamic finance. The evidence from banking, investing, takaful, and social finance points consistently in one direction: institutions that invest in genuine, independent, transparent oversight structures lower their cost of capital, attract institutional and diaspora capital, retain intellectual talent, and produce stable long-term returns. This is the baraka of governance — the compounding benefit that flows not from structural cleverness, but from structural integrity.

The path forward requires three things that the industry has consistently deferred. First, independence — Sharī'ah boards must be structurally independent from management, compensated for judgment rather than volume, and empowered to challenge rather than validate. Second, transparency — disclosure standards for Sharī'ah compliance procedures, purification ratios, tabarru' pool management, and waqf utilization must meet the threshold that institutional capital now demands. Third, accountability — governance frameworks must carry consequences, not merely recommendations.

For Islamic finance to move from a niche asset class to a global ethical benchmark, it must stop treating governance as a footnote in the annual report. The industry's founding promise was not merely transactional compliance. It was a claim about the moral quality of capital — about what money is for, and how it should be held in trust.

The question is no longer whether governance matters. The market has already answered that.

That claim will only be credible when the institutions making it are governed accordingly.

References

- Bank Negara Malaysia. Administrative Monetary Penalty — Bank Islam Malaysia Berhad, July 2025. bnm.gov.my

- Reuters. UAE Court Sentences Executives in Dubai Islamic Bank Fraud Case, 2011.

- IAIS / IFSB. Issues in Regulation and Supervision of Takaful; IFSB-8: Guiding Principles on Governance for Takaful Undertakings. iais.org / ifsb.org

- COMCEC. Improving Governance of Islamic Social Finance. comcec.org

- Journal of INCEIF. Governance Failures in Islamic Finance: The Case of Islamic Bank Ltd. journal.inceif.edu

- Salman Syed Ali. Financial Distress and Bank Failure: Lessons from Closure of Ihlas Finans in Turkey. Islamic Economic Studies, IRTI, 2007.

- Asutay et al. Causes and Solutions for the Stagnation of Islamic Banking in Turkey. Emerald Insight / IJIF, 2017. [50% market share figure]

- Grassa, R. Corporate Governance and Credit Rating in Islamic Banks: Does Shariah Governance Matters? Journal of Management & Governance, 20(4), 2016. [GCC vs. Southeast Asia credit rating differential]

- Ben Abdallah, M. & Bahloul, S. Disclosure, Shariah Governance and Financial Performance in Islamic Banks. Asian Journal of Economics and Banking, 5(3), 2021. [BOD, AC, SSB positive impact on ROA/ROE]

- Al-Smadi et al. Impact of Shariah Advisory Board Characteristics on Islamic Banks Financial Performance. Cogent Economics & Finance, 2022. [180 banks, 56 countries, 2010-2019]

- Elgattani. AAOIFI Governance Disclosure and Islamic Banks Performance. Journal of Financial Reporting and Accounting, 2020. [insignificant ROA/ROE result — cited for balance]

- Owoyemi, M.Y. Zakat Management: The Crisis of Confidence in Zakat Agencies. Journal of Islamic Accounting and Business Research, 11(2), 2020.

- Amalia et al. Good Governance in Strengthening the Performance of Zakat Institutions in Indonesia, 2018. [transparency and accountability as dominant trust factors]

- Haris, A. Enhancing Zakat Fundraising through Digital Financial Transparency. Journal of Management and Business, 2(2), 2025.

- Herbert Smith Freehills Kramer. English High Court Confirms Sharia Non-Compliance. hsfkramer.com

- International Journal of Law Management & Humanities. Governance Failures in Waqf Boards. 2025.

- Norges Bank Investment Management / Council on Ethics. Exclusion and Observation Criteria. nbim.no