GOVERNANCE AND THE BARAKA OF EDUCATION - Why Islamic Finance Education Must Embed Governance, Takaful, and Social Finance

Abstract: Islamic finance has a governance literacy problem. The industry has built $4 trillion in assets on a curriculum that largely omits the institutional architecture required to sustain them. This paper examines that gap, argues that governance must be embedded as a core discipline rather than an elective, and proposes a stakeholder-specific credential framework to close it. The chain from education to governance to pricing is traceable, documented, and correctable.

Islamic finance does not have a talent shortage. It has a governance literacy problem.

The industry has grown to over $4 trillion in assets across banking, capital markets, takaful, and social finance. The DinarStandard Top 30 Business Schools of the Islamic Economy 2026 ranking documents the educational network that has grown alongside it — from Kuala Lumpur to London, from Karachi to Riyadh. The breadth is real. So is the gap it conceals.

The graduates entering Islamic finance today can model a sukuk. Most cannot explain the governance framework that should govern the institution issuing it. They understand what Sharī'ah-compliant means. Fewer understand what Sharī'ah-governed means — and the distance between those two terms is where the industry's most consequential failures have lived.

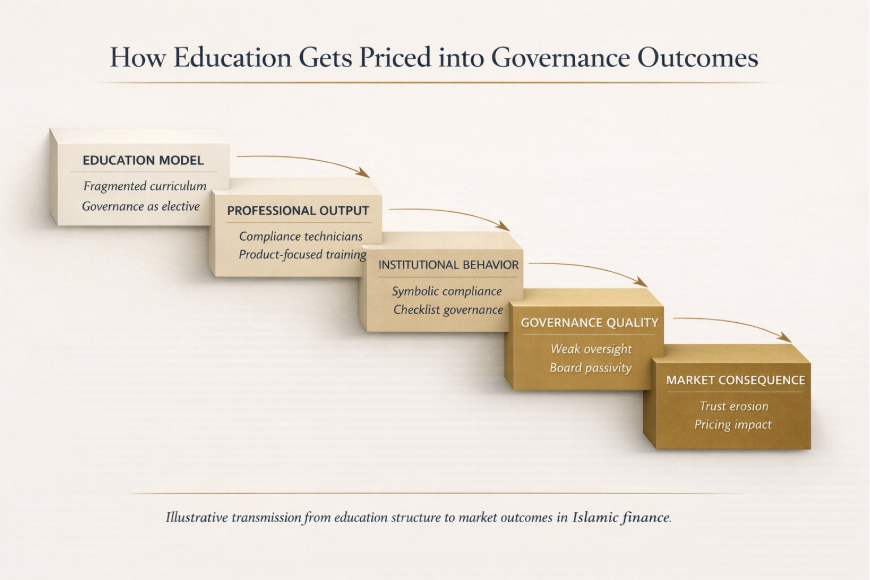

The industry is producing compliance technicians. It needs governance custodians. A compliance technician ensures a product meets a checklist. A governance custodian ensures an institution upholds the amanah — the trusteeship — that the checklist was designed to protect. One produces documentation. The other produces trust. As established in the first paper in this series, trust is now the primary pricing variable in Islamic capital markets. In practice, that trust is expressed through governance signals — board independence, disclosure quality, audit rigor, and conflict-of-interest controls — the variables capital actually prices. Education is where those signals originate.

The DinarStandard ranking reveals where the intellectual infrastructure has been built — and where the cost of not building it is now visible.

I. The Industry Is Growing Faster Than Its Talent Can Govern It

ICD-Refinitiv's Islamic Finance Development Report 2023 documents $4 trillion in global Islamic financial assets and a growth trajectory that has outpaced conventional finance across most core markets for two decades. The institutional infrastructure has followed: central bank Sharī'ah advisory councils, AAOIFI and IFSB standard-setting bodies, sovereign sukuk programs, national takaful frameworks, state-backed waqf authorities. The educational infrastructure has not.

An IFSB study on Sharī'ah governance frameworks across OIC member states identified significant variance in board independence, disclosure quality, and oversight effectiveness — variance that is not random. It correlates directly with the depth of governance education in institutions' home markets. Where universities have embedded structured governance training, institutions demonstrate stronger oversight. Where they have not, the same institutions exhibit what the literature consistently describes as symbolic compliance: board structures that satisfy formal requirements without exercising substantive judgment.

As of 2023, only 18 out of 70 countries with Islamic financial operations fully recognize AAOIFI standards — meaning that the governance frameworks those standards establish are absent or unenforced across the majority of the industry's jurisdictions. The ICD-Refinitiv Islamic Finance Development Index identifies corporate governance as the weakest pillar across its framework — the dimension on which the most financial institutions fail to meet minimum reporting standards. The literature is equally direct: the shortage of qualified Sharī'ah scholars and the concentration of a small number of senior scholars across multiple boards simultaneously are attributable, in significant part, to the absence of structured educational pathways into governance roles.

The DinarStandard ranking names the leading institutions — INCEIF, Durham University's Centre for Islamic Economics and Finance, Universiti Malaya, the Islamic University of Medina, IBA Karachi — and their achievements are genuine. But a ranking of the best schools in Islamic economics is not a ranking of the best schools in Islamic financial governance. The former is well-populated. The latter barely exists as a defined field of study.

Governance education — the deep study of AAOIFI and IFSB standards, Sharī'ah supervisory board independence, takaful participant-operator accountability, waqf stewardship ethics, and maqasid al-shariah as an applied framework — has been treated as a specialization for practitioners already in the field, not a foundation for those entering it. When governance deficiencies surface, they surface in institutions. By then, the professional pipeline has already been set.

A curriculum that treats governance as an elective produces compliance technicians. Compliance technicians staff Sharī'ah boards as credentialing exercises rather than fiduciary responsibilities. Boards that credential rather than govern produce symbolic oversight. Symbolic oversight produces institutional failures — and the pricing consequences documented in the first paper of this series: spread widening, capital flight, valuation discount. The chain begins in the lecture hall.

The industry hires for technical competence and discovers governance deficiencies only when they produce institutional failures.

II. What the Rankings Reveal — and What They Don't

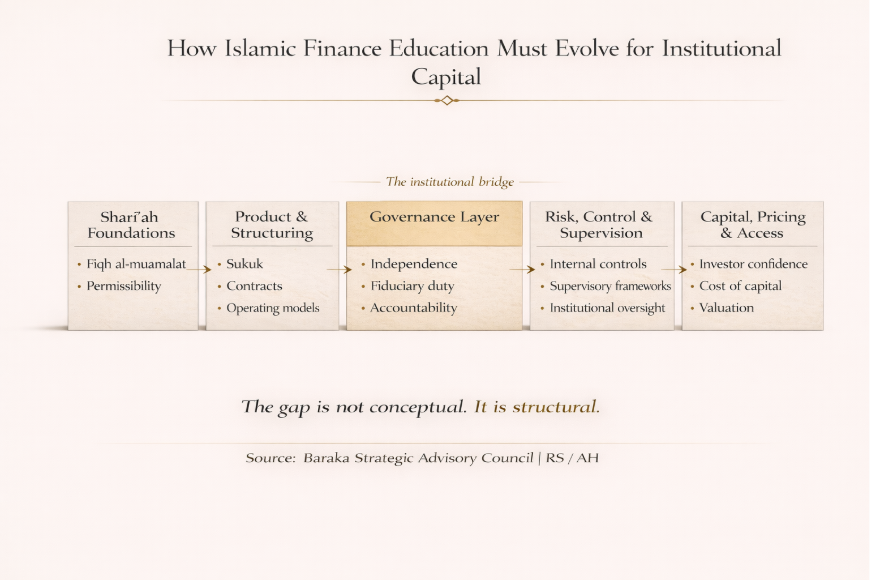

The DinarStandard Top 30 ranking evaluates business schools on Islamic economics programs, research output, industry linkages, and graduate placement. These are the right criteria for measuring academic output. They do not measure whether graduates can govern institutions — which is the capability capital ultimately prices. Program strength in Islamic economics — financial instruments, fiqh al-muamalat, Islamic macroeconomics — is not the same as program strength in Islamic financial governance. The first is well-established as a curriculum. The second remains largely absent from undergraduate and postgraduate programs at even the highest-ranked institutions.

At minimum, structured governance education requires: AAOIFI Governance Standards GS 1 through GS 22, covering Sharī'ah Supervisory Board composition, independence, internal review procedures, and ethics of financial reporting. IFSB-10 and IFSB-31, the cornerstone frameworks for Sharī'ah governance systems and their supervision. IFSB-8 on takaful governance — specifically the structural separation between participant funds and operator accounts, which the IAIS has identified as a critical unresolved constraint on sector scalability. International waqf and zakat governance frameworks, where the empirical literature identifies transparency and accountability as the dominant determinants of institutional trust. And fintech ethics — AI screening compliance, smart sukuk structuring, InsurTech for takaful — framed within maqasid al-shariah rather than treated as purely technical domains. None of this is a new curriculum. It is existing standards, applied with pedagogical intent.

Islamic finance education has been built as a linear progression from Sharī'ah foundations through product structuring — and stops there. The governance layer, which sits between what institutions know and what capital markets require, is absent. As AAOIFI Governance Standard GS 1 states: the objectives of Sharī'ah governance are not fulfilled by formality, but by accountability, independence, and transparency. That standard was written for practitioners. It reads equally well as a curriculum mandate.

The standards exist. The case studies exist. What does not exist, at the required scale, is a curriculum that treats governance as a prerequisite rather than an elective.

III. The Cost of the Gap — Symbolic Compliance and Its Consequences

The consequences of governance illiteracy in the professional pipeline are institutional, documented, and traceable to a common upstream cause. The professionals who structured the instruments, staffed the boards, and managed the institutions involved in the IBL collapse, the Ihlas failure, the DIB fraud case, and the Tabung Haji crisis were, by the standards of their training, technically qualified. What they lacked was not financial knowledge. It was governance judgment.

Symbolic compliance is the direct product of a symbolic education. When Sharī'ah boards are taught to approve rather than interrogate — when the curriculum presents board membership as a credential rather than a fiduciary responsibility — the graduates who staff those boards replicate what they were taught. AAOIFI GS 10 identifies the structural conditions under which boards cease to function as genuine oversight mechanisms: compensation tied to product approval volume, management influence over scholar selection, absence of rotation requirements. These are precisely the conditions that governance education would train practitioners to identify and resist. They persist because that education does not exist at scale.

Practitioners positioned to build the next generation of Islamic finance products — micro-takaful for underserved populations, green sukuk with genuine ESG integrity, technology-enabled waqf platforms, AI-powered Sharī'ah screening — require fluency in both the technical domain and the governance framework that gives it legitimacy. Without governance education, fintech developers build compliance tools. With it, they build trust infrastructure. The difference determines whether Islamic finance leads the ethical finance conversation or follows it.

The reputational dimension is the longest-cycle consequence. IFSB-22 identifies disclosure of governance mechanisms as central to institutional legitimacy. When professionals responsible for that disclosure cannot distinguish between a Sharī'ah board that functions and one that performs, the disclosure is inadequate by definition. Inadequate disclosure is treated as absent disclosure. The institution is priced accordingly.

The governance gap in education is not a curriculum oversight. It is a structural liability — accumulated over two decades, and now beginning to be priced.

IV. A Curriculum Architecture for Every Governance Actor

The path forward is not additional research on the governance gap. The research is sufficient. What is required is institutional commitment to closing it — and universities are the right place to lead, precisely because they sit upstream of every institutional failure the industry experiences.

Partnership models already exist. INCEIF's collaboration with Bank Negara Malaysia demonstrates that a specialist Islamic finance institution can co-design programs with a central bank regulator to produce graduates who understand governance as a supervisory imperative, not an academic concept. Durham University's Centre for Islamic Economics and Finance has shown that a Western research university can engage seriously with Islamic governance frameworks without compromising academic rigor. These are not exceptions. They are templates.

What replication requires is a stakeholder-specific credential architecture. The governance gap is not uniform across the industry — it manifests differently for scholars, regulators, takaful professionals, compliance officers, social finance practitioners, and institutional employees. A single qualification cannot address it. What the industry needs is a tiered framework: a foundation course establishing shared governance literacy across all roles, and six stakeholder-specific certificates addressing the governance demands of each role in depth.

The foundation is a Certificate in Islamic Finance Ethics and Governance — establishing amanah as organizational culture rather than personal virtue, dual-layer accountability to regulators and to Sharī'ah, the ethics of product design, and an introduction to maqasid al-shariah in daily operations. Every employee of an Islamic financial institution is a governance actor. This course ensures the culture matches the contract.

From that foundation, six stakeholder tracks address the governance demands specific to each role:

Shariah Scholars — Certificate in Shariah Board Governance and Financial Oversight. Scholars must govern, not merely opine. This curriculum addresses fiduciary duties of the SSB member, financial statement interrogation, conflict of interest protocols, fatwa documentation standards, and the structural transition from advisory to supervisory authority.¹

Regulators — Certificate in Islamic Financial Services Regulation. Regulators writing rules without understanding mudarabah create compliance theater. This curriculum covers IFSB core principles and AAOIFI enforcement frameworks, Sharī'ah non-compliance risk as systemic risk, supervising Islamic windows within conventional banks, and legal framework design for profit-and-loss sharing contracts.²

Takaful Professionals — Certificate in Takaful Governance and Participant Fund Management. Takaful's promise is mutual protection. Poor fund governance quietly betrays every participant. This curriculum addresses wakala versus mudarabah governance implications, segregation of shareholder and participant risk funds, surplus distribution policy, and operator fiduciary duty to participants.³

Compliance Officers — Certificate in Islamic Finance Compliance and Shariah Audit. Compliance without Sharī'ah literacy is box-ticking. This curriculum builds officers who understand what they are protecting: Sharī'ah audit methodology versus conventional internal audit, fatwa-to-implementation gap monitoring, disclosure frameworks, and purification of non-compliant income.⁴

Islamic Social Finance Practitioners — Certificate in Islamic Social Finance Governance and Fiduciary Practice. Zakat and waqf carry a sacred trust. Weak governance dishonors both the donor and the beneficiary. This curriculum covers fiduciary duty to zakat beneficiaries, waqf asset management and preservation, governance structures for zakat institutions and waqf boards, and ESG alignment with maqasid al-shariah.⁵

These are defined knowledge domains with existing standards, documented failure cases, and measurable competency requirements. The curriculum exists in regulatory frameworks, academic literature, and institutional case studies. What has been missing is the organizational will to treat it as a prerequisite — and the institutional architecture to deliver it at scale. These credentials are not academic enhancements. They are emerging institutional requirements for any platform seeking to attract and retain serious capital.

When that architecture is built, the downstream effects are predictable. Scholars enter boards understanding independence as a fiduciary requirement. Regulators design frameworks that reflect the structures they are supervising. Takaful operators manage participant funds with the separation IFSB-8 demands. Compliance officers distinguish between a Sharī'ah board that functions and one that performs. Social finance practitioners govern waqf assets and zakat distribution with the transparency that donor trust requires.

Education, when practiced in amanah, is not merely preparation for the industry. It is the industry's first line of governance.

The Qur'an frames the responsibility of knowledge as both warning and glad tidings. The warning is the governance gap this paper has documented. The glad tidings are the credential framework, the partnership models, and the institutional precedents that demonstrate it can be closed. The industry's response to each will determine which one defines the next decade.

One further gap deserves naming. No publication-grade practitioner survey yet exists that measures governance education deficiencies by stakeholder group — by what Sharī'ah scholars, regulators, takaful professionals, compliance officers, and social finance practitioners actually know, and what they do not. The credential architecture proposed in this paper is grounded in regulatory frameworks and institutional case evidence. It would be materially strengthened by primary survey data. That research has not been done. It is precisely the kind of infrastructure work that an independent research institute committed to Islamic capital markets governance — unaffiliated with any product issuer or institution — is positioned to undertake.

If universities do not build this into the curriculum, regulators and capital allocators will impose it in practice — through hiring standards, governance requirements, and ultimately, pricing.

Curriculum Detail by Stakeholder Track

¹ Shariah Board Governance and Financial Oversight

Fiduciary Duties of the SSB Member | Reading and Interrogating Financial Statements | Conflict of Interest Protocols and Recusal Standards | Fatwa Documentation and Minority Opinion Disclosure | From Advisory to Supervisory: Understanding the Difference

² Islamic Financial Services Regulation

IFSB Core Principles and AAOIFI Enforcement Frameworks | Sharī'ah Non-Compliance Risk as Systemic Risk | Cross-Border Regulatory Harmonization | Supervising Islamic Windows Within Conventional Banks | Legal Framework Design for Profit-and-Loss Sharing Contracts

³ Takaful Governance and Participant Fund Management

Wakala vs. Mudarabah: Governance Implications of Each Model | Segregating Shareholder and Participant Risk Funds | Surplus Distribution Policy and Board Accountability | Qard Hasan: Mechanics, Triggers, and Repayment Governance | Operator Fiduciary Duty to Participants

⁴ Islamic Finance Compliance and Shariah Audit

Sharī'ah Audit Methodology vs. Conventional Internal Audit | Fatwa-to-Implementation Gap: Monitoring Daily Transactions | Disclosure Frameworks: What Must Be Reported and to Whom | Managing and Documenting Sharī'ah Non-Compliance Incidents | Purification of Non-Compliant Income: Process and Accountability

⁵ Islamic Social Finance Governance and Fiduciary Practice

Fiduciary Duty to Beneficiaries in Zakat Distribution | Waqf Asset Management: Preservation, Investment, and Accountability | Governance Structures for Zakat Institutions and Waqf Boards | ESG Alignment with Maqasid al-Shariah | Transparency and Reporting Standards for Social Finance Entities

References

- DinarStandard. Top 30 Business Schools of the Islamic Economy 2026. Salaam Gateway Report.

- ICD–Refinitiv. Islamic Finance Development Report 2023. [Corporate governance identified as weakest IFDI pillar; $4 trillion in global Islamic financial assets]

- Grand View Research / Market Data Forecast. Islamic Finance Market Report 2024. [18 of 70 countries recognize AAOIFI standards]

- Farooq, M.O. & Zaheer, S. Shariah Governance for Islamic Finance: Challenges and Pragmatic Solutions. [Scholar shortage and concentration as educational infrastructure failure]

- Jan, S. et al. Islamic Finance Education: Current State and Challenges for Pakistan. Cogent Economics & Finance, 2023. [4 of 15 top Pakistani business schools offer Islamic finance degrees; 8 full-time faculty]

- Islamic Financial Services Board (IFSB). IFSB-10: Shariah Governance Systems for Institutions Offering Islamic Financial Services, 2009.

- Islamic Financial Services Board (IFSB). IFSB-31: Effective Supervision of Sharīʻah Governance Systems, 2023.

- Islamic Financial Services Board (IFSB). IFSB-8: Guiding Principles on Governance for Takaful Undertakings, 2009.

- Islamic Financial Services Board (IFSB). IFSB-22: Disclosures to Promote Transparency and Market Discipline for Institutions Offering Islamic Financial Services, 2019.

- Islamic Financial Services Board (IFSB). Study on Shariah Governance Frameworks across OIC Member States, 2021.

- Accounting and Auditing Organisation for Islamic Financial Institutions (AAOIFI). Governance Standards GS 1–22, 2017–2023.

- Accounting and Auditing Organisation for Islamic Financial Institutions (AAOIFI). Financial Accounting Standard FAS 1: Objectives and Concepts of Financial Accounting for Islamic Banks and Financial Institutions, 2018.

- Islamic Research and Training Institute (IRTI) & International Shari'ah Research Academy (ISRA). Waqf Core Principles and Governance Manual, 2020.

- Owoyemi, M.Y. Zakat Management: The Crisis of Confidence in Zakat Agencies. Journal of Islamic Accounting and Business Research, 11(2), 2020.

- Amalia et al. Good Governance in Strengthening the Performance of Zakat Institutions in Indonesia, 2018.

- Grassa, R. Corporate Governance and Credit Rating in Islamic Banks: Does Shariah Governance Matters? Journal of Management & Governance, 20(4), 2016.

- INCEIF / Bank Negara Malaysia. Collaboration Framework for Islamic Finance Education and Supervisory Development. bnm.gov.my

- The Noble Qur'an, Surah Yunus 10:2.