GOVERNANCE AND THE BARAKA OF GUIDANCE - Why Islamic AI Requires the Same Governance Architecture That Rescued Islamic Finance

Abstract: A new category of artificial intelligence platform has emerged, trained on Islamic texts and positioned as infrastructure for religious knowledge, financial interpretation, and Sharī‘ah compliance. These platforms represent a genuine expansion of access to Islamic knowledge. They also represent a governance gap in formation — one that Islamic finance has already lived through, and paid for. The chain of transmission that gives Islamic knowledge its authority is not a technical feature. It is the foundational legitimacy structure of the tradition. It cannot be automated without consequence. The question is not whether Islamic AI will scale. It already is. The question is whether the institutions engaging with it will demand governance architecture before, or after, the failures make it necessary.

Islamic AI has a product. It does not yet have a governance architecture.

A new category of artificial intelligence platform has emerged — trained on Islamic texts, designed to engage with religious guidance, financial interpretation, and Sharī‘ah compliance reasoning. These platforms are not peripheral experiments. They are being positioned as infrastructure: systems that interpret Islamic knowledge at scale, in real time, across the full spectrum of jurisprudence that governs Muslim life in finance, family, practice, and commerce.

The access gain is real. A practitioner in Karachi, a student in London, and a family office in Riyadh can now engage with fiqh questions, Islamic finance structuring logic, and classical scholarly interpretation through a conversational interface — without a trained scholar, a library, or a linguistic intermediary. That is not a trivial development. Accessibility has historically been among the most significant constraints on Islamic knowledge transmission.

But accessibility and legitimacy are not the same thing. And the institutions, scholars, and capital allocators now engaging with these platforms have not yet separated them.

Islamic finance once faced an identical sequence: product innovation first, governance architecture later. As documented in the first paper in this series [View], the result was institutional failures, capital flight, and a generation of eroded trust before the sector built the governance infrastructure — AAOIFI, IFSB, independent Sharī‘ah boards — that now underpins its credibility. Islamic AI is following the same sequence. The domain is broader, because it touches both capital and religious authority.

The argument is not that artificial intelligence cannot serve Islamic knowledge. It is that without governance architecture, it cannot be trusted — and trust, as this series has established, is the primary pricing variable in Islamic capital markets and the primary legitimacy variable in Islamic scholarship. When it is structurally absent, the consequences are not merely theoretical.

I. The Chain of Transmission Is Not a Technical Feature

Islamic knowledge does not derive authority from the accuracy of its content alone. It derives authority from its chain of transmission. The isnād — the documented lineage connecting a hadith back through named scholars to the Prophet — is not a metadata tag. It is the evidentiary architecture through which Islamic scholarship determines whether a narration may be relied upon. The ijaza — the license granted by a qualified scholar to a student, authorizing transmission of a text — is not a credential. It is the institutional mechanism through which Islamic knowledge passes between generations with maintained integrity.

These are not premodern administrative conventions. They are the foundational legitimacy structure of Islamic knowledge. They encode, in institutional form, the principle that authority in Islamic scholarship is not self-assigned. It is conferred — through verified chains of transmission, demonstrated competence, and recognized scholarly standing.

Current generative AI systems do not possess the equivalent of an auditable isnād. They do not hold ijāzas. Nor can their outputs be interrogated for a verified chain of transmission, because they do not have one. What they produce is not a ruling. It is a pattern — sophisticated, contextually aware, and structurally indistinguishable, in interface terms, from scholarly guidance.

That indistinguishability is the governance problem.

When a platform presents an Islamic finance compliance determination, a fatwa-adjacent response, or a Sharī‘ah screening conclusion without disclosed sources, verifiable scholarly oversight, or an auditable chain of reasoning, it may functionally approximate elements of the authority position of a Sharī‘ah board — without the independence requirements, the accountability structures, or the institutional accountability that a Sharī‘ah board carries. As AAOIFI Governance Standard GS 1 establishes: the objectives of Sharī‘ah governance are not fulfilled by formality, but by accountability, independence, and transparency. That standard was written for boards. It reads equally well as a requirement for any system that performs the function of one.

The chain of transmission that gives Islamic knowledge its authority is not a technical feature. It is the foundational legitimacy structure of the tradition — and it cannot be automated without consequence.

II. The Same Sequence That Broke Islamic Finance Is Playing Out Again

Islamic finance’s governance reckoning was not a single event. It was a sequence: rapid product innovation, governance architecture deferred, institutional failures made the absence visible, regulatory and standard-setting bodies built the architecture under pressure. The IBL collapse, the Ihlas failure, the DIB fraud — each documented in the first paper of this series — were not anomalies. They were the predictable output of an industry that treated governance as a downstream concern.

AAOIFI was established in 1990. IFSB followed in 2002. Both came after the industry had already scaled — after the failures that demonstrated, empirically, what the absence of governance architecture produces. The governance infrastructure that now underpins the sector’s institutional credibility was built reactively, not proactively. And as the second paper in this series documented, the professional pipeline that staffs the boards those bodies govern was never built at all — producing the compliance technicians who credential rather than govern, and the symbolic oversight that pricing now reflects.

Islamic AI is following the same sequence with greater speed and broader reach. The platforms have scaled. The governance architecture has not. The standard-setting bodies that should define what responsible Islamic AI governance requires — AAOIFI, IFSB, national Sharī‘ah advisory councils — have not yet produced enforceable frameworks for AI outputs in their respective domains. The scholarly oversight structures that should validate platform outputs are, where they exist, advisory rather than supervisory. The disclosure standards that would allow an institution or end user to evaluate the governance quality of an Islamic AI platform do not exist.

The IFSB has published substantive guidance on fintech and Islamic digital banking — identifying governance, risk management, and consumer protection as threshold concerns for digital Islamic financial services — in its 2020 landscape report and its 2023 Working Paper WP-27 on regulatory practices in digital Islamic banking. What it has not yet produced is an equivalent framework for AI-generated Sharī‘ah determinations — a gap that grows more consequential with each platform that scales without one.

The pattern is familiar. The window to interrupt it, before failures make interruption reactive rather than structural, is closing.

Islamic finance built its governance architecture after the failures. The question for Islamic AI is whether the same price must be paid — or whether the architecture can be built first.

III. What Happens When Algorithms Flatten Tradition

Islamic jurisprudence has, for fourteen centuries, operated through a structured tolerance for scholarly disagreement. Ikhtilāf — the tradition of principled dissent among qualified scholars — is not a weakness of the tradition. It is a feature. The four major schools of Sunni jurisprudence exist not because scholars failed to agree, but because the legal questions they were reasoning through admitted multiple defensible positions, and the tradition was wise enough to preserve the plurality rather than enforce a singular answer.

Most conversational AI interfaces default toward resolution rather than structured preservation of juristic plurality. A platform receives a question and returns an answer — singular, fluent, and presented with the confidence of a system that has processed more text than any human scholar could read in a lifetime. The mechanism that makes these systems useful in most domains — the ability to synthesize and respond — is precisely the mechanism that creates structural tension with how Islamic legal reasoning works.

The risk is not primarily that an AI platform will return an incorrect answer. Human scholars return incorrect answers; the tradition has mechanisms for correction, revision, and appeal. The risk is that an AI platform will return a confident, plausible, well-sourced-sounding answer that forecloses the interpretive plurality the tradition was designed to preserve — and that institutions relying on that output will treat it as determinative because the interface presents it that way.

In Islamic finance, the consequences are operational and measurable. A compliance determination that is incorrect does not merely mislead the professional who receives it. It potentially invalidates the transaction structured on its basis. It creates regulatory exposure for the institution that relied on it. It generates liability that cannot be unwound by a model update. The reputational consequences for an institution whose Sharī‘ah compliance was determined by an unvalidated AI output — and discovered to be wrong — are of the same class as the governance failures documented in the first paper of this series: spread-widening, institutional scrutiny, and capital re-pricing.

Hallucination — the technical term for AI-generated outputs that are confidently stated but factually or legally wrong — is a known limitation of current large language model architectures. In low-stakes domains, hallucination is a quality problem. In Islamic finance and jurisprudence, it is a governance problem. And governance problems, as this series has documented, are priced.

The risk is not that AI will get the answer wrong. The risk is that it will get the answer wrong confidently — and that the interface will not distinguish between a ruling and a pattern.

IV. Islamic Finance Built the Framework. Islamic AI Needs One.

The governance architecture that Islamic finance built — imperfectly, reactively, but consequentially — offers a template. Not a blueprint for AI governance, which requires its own domain-specific design, but a proof of concept: that an industry built on trust can create institutional infrastructure to protect that trust, and that capital markets will price the presence or absence of that infrastructure.

Governance architecture is not a brake on Islamic AI adoption. It is the condition for trusted scale.

What a governance framework for Islamic AI requires is not novel. Its components exist in the standards Islamic finance has already produced, applied to a new domain.

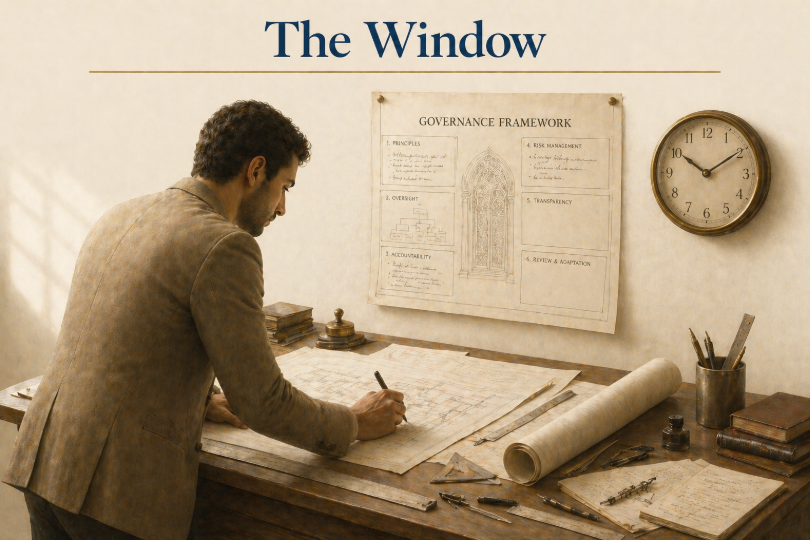

Independence is the first requirement. Sharī‘ah oversight of Islamic AI platforms must be structurally independent — not advisory, not decorative, and not subordinate to the commercial interests of the platform it governs. AAOIFI’s Sharī‘ah governance standards (GS 1 and GS 19–22) establish independence as a prerequisite for effective Sharī‘ah governance in financial institutions. The same principle applies to any system generating outputs that occupy the structural role of a Sharī‘ah determination. A scholarly advisory panel whose recommendations a platform may choose to act upon is not governance. It is symbolic oversight.

Transparency is the second — and it requires a concept the industry does not yet have a name for. This paper proposes one: the digital isnād. Not a recreation of classical hadith transmission, but its functional equivalent for AI-generated outputs: a disclosed, auditable chain establishing the authority basis of every determination a platform produces. The digital isnād is proposed as a functional governance analogy, not an equivalence to its classical form.

The digital isnād carries three dimensions simultaneously. Technically: which scholarly corpora governed the training, which methodological assumptions shape the output, and where the platform’s competence ends. Scholastically: outputs must be traceable not merely to a training dataset but to the qualified scholarly frameworks they claim to represent. A response that synthesizes multiple legal schools without disclosing the synthesis methodology is not demonstrating breadth. It is concealing the absence of a position. Regulatorily: a qualified external party must be able to trace an output to its governing principles, identify where those principles were correctly applied, and determine where they were not. AAOIFI and IFSB disclosure frameworks already establish exactly this standard for institutional Sharī‘ah oversight. The digital isnād applies that standard to the system performing the oversight function. Without it, the institution is not assessing whether an AI platform’s governance is adequate. It is assuming that it is.

Accountability is the third. The outputs of Islamic AI systems must be auditable — traceable, reviewable, and subject to correction by qualified scholarly authority. This requires not merely internal quality controls but external oversight structures: independent Sharī‘ah audit of AI outputs in governed institutional contexts, published standards for what constitutes acceptable performance, and consequences for platforms that operate outside them. Accountability without consequence is, as this series has documented from the beginning, symbolic compliance. And symbolic compliance is priced.

The governance frameworks that AAOIFI and IFSB have established for Islamic financial institutions do not cease to apply because the output is generated by an algorithm rather than a scholar. An institution that deploys Islamic AI in compliance-sensitive or jurisprudential contexts — Sharī‘ah screening, fatwa research, takaful participant communications, waqf governance documentation — without independently validated scholarly oversight, disclosed sourcing, and auditable outputs is, by the standards those bodies have already published, operating below the governance threshold they require. That is not a future regulatory question. It is a present institutional one.

The standard-setting window is open. What has not yet occurred is the institutional decision to treat Islamic AI governance as a threshold requirement rather than a future consideration. That decision becomes harder to make after the first significant failure. It is available now, before one.

The industry that builds this governance infrastructure first will not merely protect the tradition it serves. It will set the standard against which every platform that follows will be measured.

V. The Baraka of Guidance

Hidāyah — guidance — is one of the most invoked concepts in Islamic practice. It is sought in prayer, referenced in Qur’anic recitation, and understood, in the tradition, as something that flows from divine wisdom through human channels: scholars who have earned the trust to transmit it, institutions that have earned the credibility to house it, and communities of practice that have earned the standing to apply it.

Artificial intelligence can expand access to Islamic knowledge in ways that would have been unimaginable a generation ago. That is a meaningful development, and it should be treated as one. But access is not guidance. Information is not ruling. And scale is not authority.

The first paper in this series established that governance quality is the single largest non-financial driver of participation and performance in Islamic finance. The second established that governance literacy begins in the curriculum — and that what is not taught cannot be practiced. This paper adds a third dimension: governance architecture must be built into the systems the next generation of Islamic finance professionals and scholars will rely on — before those systems are treated as authoritative, not after.

The baraka of guidance is not in the speed of the answer. It is in the integrity of the chain through which it arrives.

Three requirements follow directly from the argument this paper has made. Independence: scholarly oversight of Islamic AI must be structurally embedded, not decorative — positioned upstream of outputs, not downstream of them. Transparency: source chains must be visible and auditable through a digital isnād, not concealed behind the fluency of the interface. Accountability: outputs must carry consequences — reviewable by qualified authority, correctable in practice, and subject to standards that apply to all platforms equally.

These are not aspirational principles. They are the operating requirements of any system that claims to serve the tradition of Islamic knowledge.

The first paper in this series documented what ungoverned systems produce in Islamic finance: spread-widening, capital flight, and reputational damage that does not respond to financial remedies. The governing mechanism is the same for Islamic AI. An institution whose Sharī‘ah compliance determinations, guidance outputs, or governance documentation is generated by a platform without independent scholarly oversight and a digital isnād has not outsourced its compliance function. It has unsecured it. The market will eventually price that exposure — as it has priced every equivalent governance gap this series has documented.

The question is not whether Islamic AI may become infrastructure for the Ummah. The question is whether it will become governed infrastructure — or whether the industry will wait, as it has before, for the failures to make governance necessary.

Authority in Islamic tradition is not conferred by scale. It is earned through chains of transmission, institutional integrity, and the long-run credibility that comes only from being answerable — to scholars, to institutions, and to the communities relying on the guidance being given.

References

• Siddiqui, R. & Hammad, A. Governance and the Baraka of Trust. Baraka Strategic Advisory Council, 2025. [Article 1 in this series]

• Siddiqui, R. & Hammad, A. Governance and the Baraka of Education. Baraka Strategic Advisory Council, 2025. [Article 2 in this series]

• Accounting and Auditing Organization for Islamic Financial Institutions. Governance Standards, including GS 1 and GS 19–22 on Sharī‘ah Governance. Issued/revised 2024.

• Islamic Financial Services Board. IFSB-10: Sharī‘ah Governance Systems for Institutions Offering Islamic Financial Services. Kuala Lumpur: IFSB, 2009.

• Islamic Financial Services Board. IFSB-31: Guiding Principles for Effective Supervision of Sharī‘ah Governance. Adopted July 2025.

• Islamic Financial Services Board. Fintech and Islamic Finance: Current Landscape and Future Outlook. Kuala Lumpur: IFSB, 2020.

• Islamic Financial Services Board. Regulatory Practices in Digital Islamic Banking. Working Paper WP-27. Kuala Lumpur: IFSB, December 2023.

• Brown, T. et al. Language Models are Few-Shot Learners. Advances in Neural Information Processing Systems (NeurIPS), 2020.

• Ji, Z. et al. Survey of Hallucination in Natural Language Generation. ACM Computing Surveys, 55(12), 2023.

• Kamali, M. H. Principles of Islamic Jurisprudence. Islamic Texts Society, 3rd ed., 2003.

• Hallaq, W. B. An Introduction to Islamic Law. Cambridge University Press, 2009.

• Grassa, R. Corporate Governance and Credit Rating in Islamic Banks: Does Shariah Governance Matters? Journal of Management & Governance, 20(4), 2016.

• Accounting and Auditing Organization for Islamic Financial Institutions. Governance and Ethics Board. Exposure Draft: Governance Standard on Islamic Crowdfunding. Manama: AAOIFI, 2021. [AAOIFI’s fintech governance work is ongoing; no standalone AI governance standard has been issued as of 2025 — which is the institutional gap this paper identifies.]