Islamic Governance in the VC Ecosystem, Beyond Due Diligence

1. Reframing the question

Recent collapses and crises across the venture world — from failed "halal fintechs" to collapsed ethical startups — have reignited a familiar debate: how should Islamic finance align with ESG, sustainability, impact, and governance frameworks?

In reality, the question is framed wrong.

For Islamic finance, these frameworks — environmental responsibility, social justice, fiduciary integrity, intergenerational stewardship, transparency — are not imported values. They are already embedded within the maqasid al-shariah, the protected ends of the Shariah:

- Faith (din) provides the ethical anchor — the threshold within which the rest operates.

- Life and lineage carry environmental and intergenerational responsibility.

- Intellect underpins transparency and knowledge governance — the prohibition of gharar and the duty of clear disclosure.

- Wealth embodies fiduciary and risk-management discipline — the original prohibition of waste, exploitation, and ruinous speculation.

These are not parallel value sets. They form an integrated governance architecture that produces environmental, social, and ethical safeguards as natural outputs of a coherent moral system.

The challenge, then, is not conceptual. It is linguistic and operational — translating an internally consistent Islamic governance logic into measurable structures within venture capital, in the vocabulary that DFIs, sovereigns, and institutional limited partners read in.

2. From due diligence to continuous stewardship

Most venture funds, even those calling themselves "Islamic," still treat due diligence as a snapshot before investment — a compliance hurdle rather than a living process.

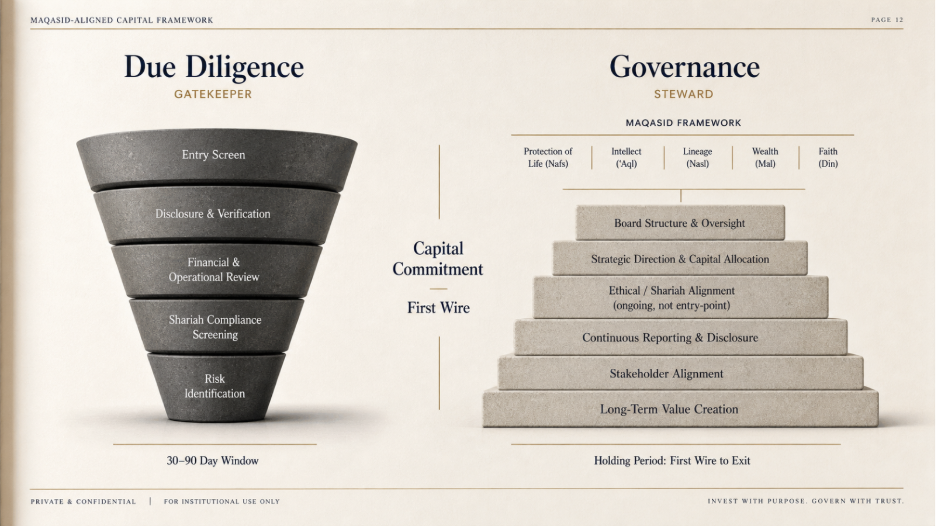

True Islamic governance begins at due diligence but extends throughout the investment lifecycle, from the initial Shariah foundation to a faithful exit. The contrast is structural, not merely a matter of duration: due diligence narrows toward a single decision point; governance ascends through the holding period, built on a maqasid foundation, accumulating obligations rather than discharging them.

Exhibit 1. Due Diligence as Gatekeeper, Governance as Steward.

The funnel and the stairs are not two phases of the same process. They are two different shapes of accountability. Due diligence terminates; governance does not.

3. A maqasid-aligned governance architecture

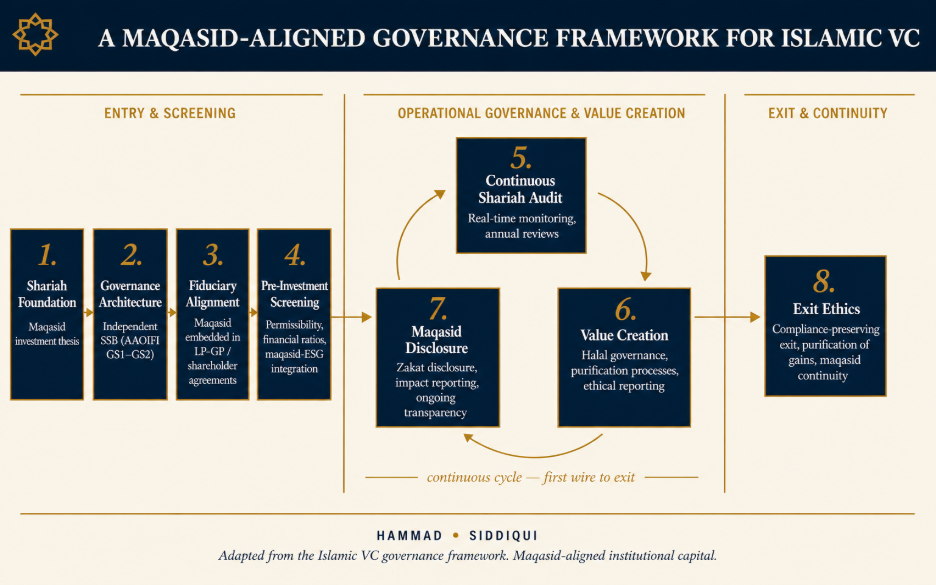

What does it look like, in practice, to translate the maqasid into a venture governance architecture? The framework below sets out eight steps across three bands — entry and screening, operational governance and value creation, and exit and continuity.

Step 1. Shariah Foundation — the maqasid investment thesis. Every fund should define its thesis in maqasid terms, ensuring investments uphold the protected ends. At this foundation, sustainability, ESG, and impact become expressions of these ends, not external imports.

Step 2. Governance Architecture — building the supervisory backbone. An independent Shariah Supervisory Board, structured in line with AAOIFI Governance Standards GS1 and GS2, must guide fund decisions and review contracts and structures across the lifecycle.

Step 3. Fiduciary Alignment — embedding governance in the legal DNA. Embed Shariah responsibilities into shareholder agreements, LP-GP contracts, and investment policies — making governance a binding fiduciary obligation, not rhetoric. This is the move that prevents Shariah from sitting as a marketing layer above a conventional cap stack.

Step 4. Pre-Investment Screening — integrated filters. Shariah due diligence combines conventional metrics (market, product, team) with Islamic screens (business permissibility, financial-ratio tests) and ESG–impact alignment guided by maqasid principles. This is where alignment is verified, not where it ends.

Step 5. Continuous Shariah Audit. Governance continues beyond deal closure. Funds should implement continuous Shariah audits, internal reviews, and real-time monitoring — maintaining ethical accountability and investor trust across the holding period.

Step 6. Value Creation — operationalizing halal governance. VCs must help portfolio companies internalize halal governance through purification processes, Shariah risk management, and ethical reporting systems — institutionalizing faith as a leadership discipline rather than a brand attribute.

Step 7. Maqasid Disclosure — making integrity visible. Public sharing of Shariah audit results, governance disclosures, zakat treatment, and impact metrics — making moral accountability both visible and verifiable.

Step 8. Exit Ethics — upholding compliance to the end. Exits must preserve Shariah integrity:

- No sale to non-compliant acquirers.

- Purification of gains before distribution.

- Transparent record of Shariah review at closure.

Exit ethics prevent moral erosion at the point of profit-taking — the moment when the temptation to relax governance is greatest.

Exhibit 2. The eight-step maqasid-aligned governance framework.

4. Why this matters now

When Islamic angel investors and venture capitalists talk about due diligence, what they very often actually mean is governance. The conflation is consequential.

The recent record makes the cost hard to ignore. The Dana Syariah case — disclosed in February 2026 by DinarStandard analyst Ali AlGhofiqi in Salaam Gateway and now described as one of the largest Islamic fintech crises globally — is the most direct illustration. Dana Syariah was a Sharia-compliant peer-to-peer real estate platform in Indonesia, founded in 2017 and licensed by Otoritas Jasa Keuangan (OJK), which channeled approximately $250 million from more than 41,500 investors. The platform reported a 99.82% 90-day repayment success rate (TKB90) for months while withdrawals were already suspended. After regulatory pressure, the figure was revised to 6.92%. Indonesian National Police investigators subsequently announced that 99 of 100 projects underwriting investor capital were allegedly fictitious. One of the company's founders served, simultaneously, as deputy head of the Indonesian Fintech Lending Association's Shariah fintech funding cluster — the self-regulatory body to which OJK delegates monitoring.

This is what the failure mode looks like priced in retrospect: licensure, brand ambassadors, awards, public claims of collateralization, and a Shariah label — without continuous Shariah governance, transparent disclosure, or independent oversight that survived the entry screen.

Dana Syariah is not isolated. The Indonesian eFishery case from 2025 — a once-celebrated impact venture, founder convicted of large-scale investor fraud, capital raised under sustainability and ethical-finance narratives — illustrates the same pattern from outside the explicitly Shariah-aligned segment. The Global Islamic Fintech Report 2025/26 (DinarStandard and Elipses) ranks Indonesia as the world's fourth most robust Islamic fintech ecosystem — a position now meaningfully under question. The academic and industry literature has been warning for years that the sector's most serious risk is not the absence of Shariah-compliant products but the absence of continuous Shariah governance behind them. Habib Ahmed has written on the structural difficulty of embedding Shariah supervision in fintech operations that move faster than traditional supervisory boards can evaluate. Noor Suhaida Kasri has documented the pattern of regulatory arbitrage across jurisdictions. Amjad Hussain at K&L Gates has publicly argued that Shariah governance must be embedded from the first term sheet rather than added on at product level. The IFSB and AAOIFI joint work on standardization sits on the same diagnosis.

The verdict the literature is converging on is consistent: Shariah governance weaknesses remain systemic. Startups often treat compliance as a brand asset rather than a fiduciary discipline. Shariah boards screen at entry and go quiet. Investor oversight structures exist on paper. Alignment is treated as a moment rather than a posture. And then, periodically, a public failure forces a reckoning — and the question that should have been asked is governance, not due diligence. Performing due diligence at entry is insufficient if post-investment governance is absent.

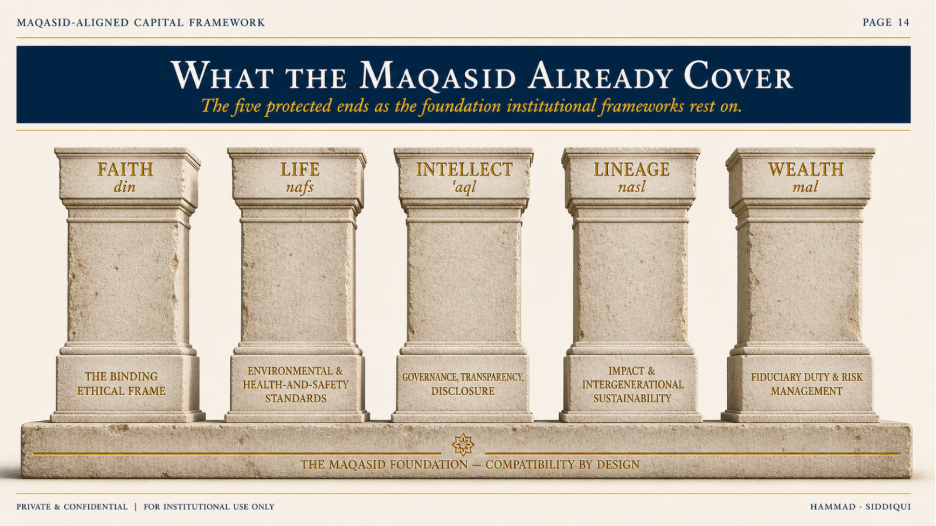

5. Beyond convergence: compatibility by design

Exhibit 3. What the maqasid already cover.

Islamic governance does not approximate ESG through convergence — it achieves compatibility by design. When faithfully implemented, the maqasid-based model produces sustainability, transparency, and fiduciary integrity as organic outputs, not borrowed criteria.

Global investors, DFIs, and sovereign funds already understand ESG, IFRS, and IFC standards. The Islamic VC community's task is to translate maqasid coherence into those vocabularies — measurable metrics, recurring audits, transparent disclosure — without flattening its moral depth into a checkbox exercise.

6. Stewardship as the governance standard

In the Islamic venture ecosystem, due diligence is the entry point, not the endpoint. The real test of Islamic governance is the fund's ability to uphold amanah (trust) and adl (justice) through the exit and beyond.

A serious Shariah-aligned VC fund must therefore:

- Treat governance as a continuous posture, not a transaction.

- Provide Shariah audit continuity throughout its portfolio companies.

- Embed maqasid metrics alongside return metrics.

- Align profit with purpose, and exit with ethical closure.

Only then will Islamic VC transcend compliance marketing and embody its true spirit — fiduciary stewardship under faith, producing governance that is not borrowed but authentically Islamic.